- What Does Third Party Insurance Mean?

- Is Third Party Car Insurance Mandatory in the UAE?

- Third Party Car Insurance Premiums in the UAE

- How Does Third Party Car Insurance Work? Simple Examples

- What is Covered Under Third Party Car Insurance UAE?

- What is Not Covered Under Third Party Car Insurance?

- Add-ons You Can Consider With Third Party Car Insurance

- Third Party Insurance vs Comprehensive Car Insurance

- Who Should Buy Third Party Car Insurance in the UAE?

- Top Insurers Offering Third Party Car Insurance in the UAE

- Cheapest Third Party Car Insurance in the UAE: What Affects the Price?

- Best Third Party Insurance for Car: How to Choose the Right Plan?

- Documents Required to Buy Third Party Car Insurance in the UAE

- How to Claim Third Party Insurance After an Accident?

- Third Party Claim Rights in the UAE: What Can the Injured Party Do?

- Replacement Car or Loss of Benefit in Third Party Claims

- How Do Depreciation and New Parts Work in Third Party Claims?

- Sources

- FAQs on Third Party Car Insurance in the UAE

- Know More About Car Insurance

Third Party Car Insurance

Third party car insurance in the UAE is the most basic motor insurance cover you can buy. It protects you financially if your car causes ...read more

Get 12 Free Car Washes

Search Your Car's brand

Nissan

Toyota

Honda

Mitsubishi

Ford

Hyundai

4.6/5

37,550

35+

Insurance Partners

2 Million+

Trusted Customers

1 Million+

Policies Sold

This type of policy is usually cheaper than comprehensive insurance, which is why many drivers choose it for older or lower-value cars. Still, the cheapest option is not always the smartest one, so it is important to know what is covered, what is excluded, and when you may need extra coverage.

What Does Third Party Insurance Mean?

|

Quick Answer: What is Third Party Car Insurance in the UAE? Third party car insurance is the most basic motor insurance cover. It pays for damage or injury caused to someone else because of your insured vehicle. This can include damage to another car, damage to someone’s property, or bodily injury caused to a third party. |

In car insurance, ‘third party’ simply means the other person affected by your car. It could be another driver, a passenger, a pedestrian, a shop owner, or anyone whose property gets damaged because of an accident involving your insured vehicle. Here is an easy way to understand it —

| Party | Meaning |

|---|---|

| First party | You, the car owner or policyholder |

| Second party | The insurance company |

| Third party | The other person who suffers injury, death or property damage |

So, third party insurance for a car is a policy that covers your legal liability towards that other person. For example, if your car hits another vehicle, your third party insurance can pay for the other vehicle’s repair. But it will not pay for your own car’s repair. This is why third party car insurance is often called a liability-only cover. It protects you against claims from others, not against losses to your own vehicle.

Third Party Car Insurance Plans in UAE - 2026

Some of the best and the cheapest car insurance quotes in Dubai are:

*Above mentioned prices are for Honda City EX 1.5L, 2022 model.

Table of Content

Is Third Party Car Insurance Mandatory in the UAE?

Yes, third party car insurance is mandatory in the UAE. You cannot legally drive or register a car without valid motor insurance in UAE. It is the minimum level of insurance required for vehicle owners. You can choose a higher level of protection with comprehensive car insurance, but you cannot go below third party cover. So, if you are looking for a basic and budget-friendly policy, third party insurance is the starting point.

Third Party Car Insurance Premiums in the UAE

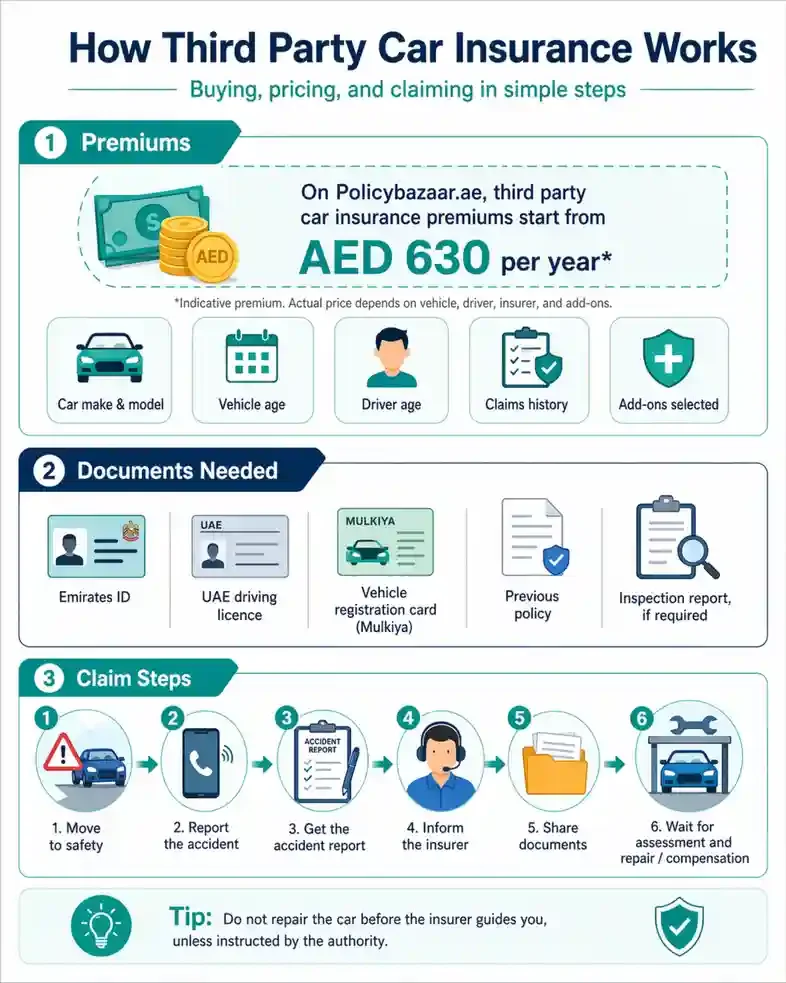

Third party motor insurance is usually the most affordable type of vehicle coverage in the UAE. On Policybazaar.ae, third party car insurance تأمين السيارات premiums start from AED 630 per year*, making it a practical option for those who want basic cover at a lower cost. You can compare third party car insurance plans on Policybazaar.ae and check quotes from multiple insurers in one place. This helps you choose a plan that fits your budget without missing important details like claim support, liability limits, and optional benefits.

*Premiums are indicative and may change as per insurer, vehicle details, driver profile, and chosen coverage

How Does Third Party Car Insurance Work? Simple Examples

Third party car insurance works when your insured car causes loss or damage to someone else. Your insurer handles the third-party claim as per the policy terms, limits, and exclusions.

Here are a few straightforward examples —

Example 1: You hit another car

You accidentally hit another car at a traffic signal:

- The other car’s repair may be covered

- Your own car’s repair will not be covered

- You will need to pay for your own damage unless you have comprehensive insurance

Example 2: Your parked car damages another vehicle

Your parked car rolls back and hits another car:

- The other car’s damage may be covered

- Your own car’s damage will not be covered

- The claim will depend on the police report and policy terms

Example 3: You damage someone’s property

You lose control and accidentally hit a shopfront, villa gate, wall, or roadside pole:

- Third party insurance may cover the damage caused to that property

- Your own car damage will not be covered

- The insurer will check the accident report and claim documents before processing it

Example 4: A permitted driver causes an accident

Someone drives your car with your permission and causes an accident:

- The third-party loss may be covered

- The driver should have a valid UAE driving license for that vehicle category

- If the driver is not legally allowed to drive, the insurer may reject the claim or recover the paid amount later

What is Covered Under Third Party Car Insurance UAE?

Third party car insurance mainly covers the loss or damage caused to another person due to your insured vehicle. The cover usually applies when your car causes injury, death, or property damage to a third party.

| What is Covered in Third-Party Insurance | What it Means | Example |

|---|---|---|

| Third-party property damage | Damage caused to someone else’s car, building, shop, wall, fence, or other property | You hit another car at a traffic signal and damage its bumper |

| Third-party bodily injury | Physical injury caused to another person due to an accident involving your insured car | Your car injures a pedestrian or another driver |

| Third-party death liability | Compensation linked to death caused to a third party in an accident | A serious accident leads to loss of life |

| Damage caused while using the vehicle | Accidents that happen while the car is being driven, moved, parked, or used | Your parked car rolls and hits another vehicle |

| Liability of a permitted driver | Cover may apply when someone else drives your car with your permission, as long as they hold a valid license for that vehicle category | Your spouse drives your car and causes damage to another vehicle |

What is Not Covered Under Third Party Car Insurance?

Third party motor insurance does not cover your own losses. It only covers the loss caused to another person or their property because of your insured vehicle.

Here are the common things not covered under a basic third party car insurance policy —

| Not Covered in Third Party Insurance | What it Means |

|---|---|

| Damage to your own car | If your car is damaged in an accident caused by you, the repair cost is not covered |

| Theft of your car | If your car is stolen, third party insurance will not pay for it |

| Fire damage to your car | Damage due to fire is not covered unless you have a wider cover or add-on |

| Natural disaster damage | Damage due to flood, storm, rain, or other natural events is not covered under basic third party cover |

| Personal belongings | Items kept inside your car, such as laptop, phone, bag, or sunglasses, are not covered |

| Own windscreen or tyre damage | Damage to your own windscreen, tyres, or parts is not covered |

| Personal injury to driver | Injury to the driver is not usually covered unless a personal accident add-on is included |

| Passenger injury add-on | Passenger cover may need to be added separately, depending on the policy |

| Off-road damage | Damage while driving off-road is not covered unless the policy clearly includes it |

| Agency repair for your car | Since your own car damage is not covered, agency repair is not included |

Example of 3rd Party Car Insurance —

You hit another car in Sharjah. The other car’s door is damaged and your front bumper is also broken. Your third party insurance can help cover the other car’s repair, but you will have to pay for your own bumper repair.

Add-ons You Can Consider With Third Party Car Insurance

Basic third party car insurance gives limited protection. It covers your liability towards others, but it may not cover you, your passengers, or your car. This is why some insurers offer add-ons at an extra cost. You can check for these add-ons before buying —

- Personal accident cover for driver — Helps cover injury or death of the driver, as per policy terms

- Personal accident cover for passengers — Gives extra financial protection for passengers travelling in the insured car

- Roadside assistance — Useful if your car breaks down, gets a flat tyre, has a battery issue, or needs towing

- Oman extension — Helpful if you drive from the UAE to Oman and want cover across the border

- Rent-a-car or courtesy car benefit — Some insurers may offer a temporary replacement car or cash benefit while the car is under repair

- Natural disaster cover — Some plans may offer extra protection for flood, storm, or similar events

|

Quick Tip - Do not add every benefit without checking. Pick the ones that match how you drive. For example, if you drive daily or travel long distances, roadside assistance can be useful. If you often travel with family, personal accident cover for passengers may be worth checking. |

Third Party Insurance vs Comprehensive Car Insurance

Both third party insurance and comprehensive insurance cover you on the road, but they work very differently.

Source: AI Generated/Human Edited

| Feature | Third Party Car Insurance | Comprehensive Car Insurance |

|---|---|---|

| Basic purpose | Covers your liability towards others | Covers third-party liability and your own car damage |

| Legal requirement | Meets the minimum insurance requirement | Also meets the legal requirement |

| Damage to another car | Covered | Covered |

| Injury to a third party | Covered | Covered |

| Damage to your own car | Not covered | Covered, subject to policy terms |

| Theft of your car | Not covered | Usually covered |

| Fire damage to your car | Not covered | Usually covered |

| Natural disaster damage | Not covered under basic third party cover | May be covered, depending on the policy |

| Premium | Usually cheaper | Usually higher |

Which One Should You Choose?

Choose third party insurance if your car is old or has a low market value, or you only want basic cover at a lower price. Choose comprehensive insurance if your car is new, expensive, financed, or costly to repair. It may cost more, but it gives better peace of mind because your own car is also protected.

Who Should Buy Third Party Car Insurance in the UAE?

Third party car insurance is a good choice for individuals who want basic cover at a lower cost. It works best when the car is not very expensive to repair or replace. You can consider third party insurance if:

- Your car is old and has a low resale value

- You want the minimum required motor insurance

- You don’t drive the car very often

- You are comfortable paying for your own car repairs

- You want a budget-friendly policy for basic road protection

However, third party insurance may not be the right choice for every driver/car owner. It may not be suitable if:

- Your car is new

- Your car is expensive or luxury

- Your repair costs are usually high

- Your car is financed by a bank

- You drive daily in busy areas

- You want cover for theft, fire, flood, or own damage

Top Insurers Offering Third Party Car Insurance in the UAE

Some popular insurers you can compare include —

- Sukoon Insurance

- GIG Gulf

- RAK Insurance

- Orient Insurance

- Al Wathba National Insurance

- Dubai National Insurance & Reinsurance

- Insurance House

- Adamjee Insurance

Cheapest Third Party Car Insurance in the UAE: What Affects the Price?

Third party car insurance is usually cheaper than comprehensive insurance because it does not cover your own car damage. Still, the price can change from one driver to another. The cost may depend on —

- Car make and model — Some cars cost more to insure because of higher repair costs, engine size, or claim history

- Vehicle age — Older cars are often insured under third party cover, but premiums can still vary

- Driver’s age — Young or new drivers may get higher quotes

- Driving experience — More driving experience can sometimes help you get a better premium

- Claims history — A clean record may help reduce the cost

- Emirate of registration — The price may differ for cars registered in Dubai, Abu Dhabi, Sharjah, or other emirates

- Add-ons selected — Extra covers like roadside assistance or personal accident cover can increase the final price

Should You Choose the Cheapest Third Party Car Insurance in Dubai?The cheapest third party car insurance in the UAE is not always the best option. Before buying, check —

A low premium is useful, but a smooth claim experience is more important when an accident actually happens. |

Best Third Party Insurance for Car: How to Choose the Right Plan?

The best third party insurance for a car is not always the cheapest one. A good policy should give you the right liability cover, clear terms, and simple claim support. Before buying a plan, check —

- Third-party property damage limit — See how much the insurer will pay if your car damages another vehicle or someone’s property

- Bodily injury cover — Check how the policy handles injury or death caused to a third party

- Claim process — A good insurer should have a clear and easy claim process

- Garage network — Check if the insurer has a wide approved garage network

- Roadside assistance — Some third party plans offer it as an add-on or benefit

- Personal accident cover — You may be able to add cover for the driver and passengers

- Policy exclusions — Read what is not covered before buying

- Customer support — Choose an insurer that is easy to reach during emergencies

- Premium vs benefits — Do not compare only the price; compare what you get for that price

|

Quick Tip! - If two plans have almost the same premium, choose the one with better claim support, higher liability limits, and useful add-ons. A cheap policy can save money today, but a weak claim process can create problems later. |

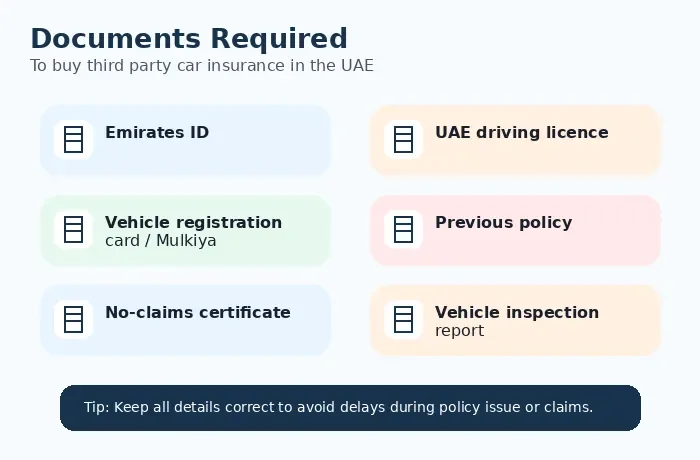

Documents Required to Buy Third Party Car Insurance in the UAE

To buy third party car insurance in the UAE, you need to share basic personal, driving, and vehicle details. The exact list can change slightly from one insurer to another, but most insurers ask for the following —

Source: AI Generated/Human Edited

- Emirates ID - Used to verify your identity and UAE residency details

- UAE driving license - Required to check whether you are legally allowed to drive the vehicle category you want to insure

- Vehicle registration card or Mulkiya - This has important vehicle details like registration number, chassis number, engine number, make, model, and year

- Previous insurance policy - Usually needed at the time of renewal or when switching from one insurer to another

- No-claims certificate - If you have not made claims in previous years, this may help you get a better premium

- Vehicle inspection report - This may be required if the policy has expired, the car is old, or the insurer asks for it before issuing cover

- Car purchase documents - For a newly bought used car, you may need a sale agreement, transfer documents, or other vehicle ownership proof

Documents Required for Car Insurance in UAE

How to Claim Third Party Insurance After an Accident?

If you meet with an accident in the UAE, do not leave the spot without reporting it. Even a small accident usually needs an official accident report before the insurance claim can move ahead. Here’s what you should do —

- Move to a safe place, if possible - If the car can be moved and there is no serious injury, shift it away from traffic.

- Check if anyone is injured - If there is injury, call emergency services immediately.

- Report the accident - Contact the police or use the approved accident reporting service in that emirate. You will need an official accident report for the claim.

- Inform the insurer - Call your insurance company or submit the claim online, depending on the insurer’s process.

- Share the required documents - Usually, you may need the accident report, driving licence, Emirates ID, vehicle registration card, and insurance policy copy.

- Follow the claim instructions - The insurer will guide you on the next step. If you are the third party affected in the accident, the at-fault driver’s insurer may handle your claim.

- Wait for the claim assessment - The insurer may inspect the vehicle, check the police report, review liability, and then process the repair or compensation.

|

Quick Tip - Don’t repair the vehicle before the insurance process starts, unless the insurer or authority tells you to. Repairs done without approval may create problems during claim settlement. |

Third Party Claim Rights in the UAE: What Can the Injured Party Do?

If another driver damages your car or property, you become the third party in the claim. This means you can raise a claim against the at-fault driver’s insurance company. Here’s what you can usually do —

- Collect the accident report: The police report or approved accident report will mention who was at fault. This is the most important document for the claim.

- Contact the at-fault driver’s insurer: Once you have the report, you can approach the insurance company of the driver who caused the accident.

- Submit your documents: You may need your Emirates ID, driving license, vehicle registration card, accident report, and photos of the damage.

- Get the vehicle inspected: The insurer may ask you to visit an approved garage or assessment centre.

- Wait for repair approval or compensation: The insurer will review the documents and check the damage. It’ll then process the claim as per policy terms.

- Ask for updates: Keep your motor insurance claim number safe and follow up with the insurer if there is a delay.

Replacement Car or Loss of Benefit in Third Party Claims

In some third party claims, the injured person may get a replacement car or a cash amount for the period their car is under repair. This is usually called loss of benefit or substitute vehicle allowance. This benefit is not for the driver who caused the accident. It is mainly for the third party whose car was damaged because of someone else’s mistake. Here’s how it may work —

- If your car is damaged by another driver: You can file a third party claim with the at-fault driver’s insurer

- If your car needs repairs: The insurer may arrange a replacement car or pay a daily allowance, depending on the policy terms

- If your car is not usable: This benefit can help you manage your daily travel while your car is being repaired

- If the insurer offers cash instead of a car: The amount and number of days will depend on the policy wording and claim approval

- If the repair takes longer: The approved benefit may still have a maximum limit, so check the policy terms

Simple Example - Your car is hit by another driver in Abu Dhabi and the accident report shows that the other driver is at fault. Your car needs 7 days of repairs. In this case, the at-fault driver’s insurer may provide a replacement car or a cash allowance for the approved repair period, subject to the policy terms.

How Do Depreciation and New Parts Work in Third Party Claims?

In a third party claim, the insurer’s job is to bring the damaged vehicle back to its pre-accident condition. This can be done through repair, replacement of damaged parts, cash settlement, or total loss settlement, depending on the case. But there is one important point many car owners miss: depreciation.

Depreciation may apply when the injured third party asks for new parts instead of the damaged used parts. In that case, the injured third party may have to bear the depreciation percentage as per the policy schedule.

How Does it Usually Work?

- If the vehicle is less than one year old, damaged parts are generally replaced with new original parts without depreciation deduction for the injured third party.

- If the vehicle is older than one year, the insurer may repair it at a suitable repair shop based on the car’s type and year of manufacture.

- The damaged parts may be replaced with parts of the same standard.

- If the injured third party specifically asks for brand-new parts, depreciation may apply.

- Some safety-related parts may need to be replaced with new ones without depreciation deduction. This depends on the policy schedule.

Sources

- Central Bank of the UAE / Unified Motor Vehicle Insurance Policy Against Third Party Liability

- Policy wordings of major insurers: Sukoon, Al Wathba, RAK Insurance, Dubai National Insurance, Insurance House, Adamjee, and more

- Official insurer pages where needed

FAQs on Third Party Car Insurance in the UAE

What is third party car insurance?

Third party car insurance is a basic motor insurance policy that covers damage, injury, or death caused to another person due to your insured vehicle. It does not cover damage to your own car.

Is third party car insurance mandatory in the UAE?

Yes, third party car insurance is mandatory in the UAE. You need valid motor insurance to drive, register, or renew your car.

What does third party car insurance cover?

It usually covers third-party property damage, bodily injury, and death caused by the insured vehicle, subject to the policy terms and limits.

Does third party insurance cover my own car?

No, third party insurance does not cover damage to your own car. If you want cover for your own vehicle, you should consider comprehensive motor insurance.

Is third party insurance cheaper than comprehensive insurance?

Yes, third party insurance is usually cheaper because it gives limited cover. It mainly protects you against claims made by others, not your own vehicle damage.

What is the cheapest third party car insurance in the UAE?

The cheapest third party car insurance depends on your car, driving history, age, emirate, and insurer. On Policybazaar.ae, car insurance premiums start from AED 630 per year.

Can I buy third party car insurance online in Dubai?

Yes, you can buy third party car insurance online in Dubai. You can compare plans, check premiums, upload documents, and buy the policy online.

Which is the best third party insurance for a car?

The best third party insurance is the one that gives the right liability cover, easy claims support, useful add-ons, and a fair premium. Do not choose only by the lowest price.

What documents are required for third party car insurance?

You may need your Emirates ID, UAE driving licence, vehicle registration card or Mulkiya, previous policy, and vehicle inspection report if required.

Can I add roadside assistance to third party insurance?

Yes, some insurers offer roadside assistance as an add-on with third party car insurance. It can help with towing, flat tyre, battery issues, and breakdown support.

Does third party insurance cover passengers?

Basic third party insurance may not cover the driver or passengers in your own car. You may need to add personal accident cover for the driver and passengers.

Is third party insurance enough for an old car?

It can be enough if your car has a low market value and you are comfortable paying for your own repairs. If repair costs are still high, comprehensive insurance may be safer.

Popular Car Insurance in UAE

Know More About Car Insurance

Other Insurance Products - Health Insurance Dubai | Best health Insurance in UAE | Health Insurance Cost in UAE | Term insurance Dubai | Life insurance UAE | Term insurance For NRI | Best Monthly investment Plan UAE | Investment Plans UAE | Top Mutual Funds UAE | Child Education Plan UAE | Online Trading in UAE | Travel Insurance | Home Insurance Dubai | Group Medical Insurance | Business Insurance Dubai | Contents Insurance Dubai | Workers Compensation Insurance

Nupur Jain

Aadil KhanDubai, 31 March 2023

★★★★★

Affordable Premium!Got an affordable premium on the TPL car insurance with a comprehensive third-party car coverage.

Adam Dubai, 14 March 2023

★★★★★

Recommend policybazaar.ae for TPL car insuranceI recently purchased a third party liability (TPL) car insurance plan from policybazaar.ae and was pleased with the experience. The process of purchasing the insurance was straightforward and the customer service team was helpful and efficient. I appreciate the more affordable price of TPL insurance compared to comprehensive coverage and feel confident in the protection it provides for damages or injuries to other vehicles or property in the event of an accident. Overall, I would recommend policybazaar.ae for TPL car insurance.

Faiz SayedDubai, 28 January 2023

★★★★★

Renewed my TPL car insurance on Policybazaar!I was looking for a good TPL in Dubai online when I came across Policybazaar. The website listed the best TPL insurance plans from the leading providers. I studied every plan and managed to secure the plan that meet my needs. I highly recommend people to use this website to get great deals on car insurance plans.

FARAZ AFZALDubai, 26 January 2023

★★★★★

Got TPL Insurance Plans at Affordable Premium!I managed to purchase a TPL from Policybazaar at an affordable premium. I landed on Policybazaar after doing an extensive search for the insurance plan. The plan covers the third-party vehicle comprehensively. This has given me peace of mind while I drive around in Dubai.

Bashar AbdelrahmanDubai, 3 January 2023

★★★★★

Policybazaar UAE for the Best TPL car insurance plans!I was disappointed with my previous TPL car insurance provider as the third-party cover provided was way less than what was written on paper. Once my term ended, I decided to switch providers. As I was browsing for options online, I came across Policybazaar. This portal helped me compare the plans and get my doubts about TPL insurance cleared. I managed to fund the best TPL car insurance plan from a better provider. I even received a special discount on premiums from Policybazaar. All in all, it was a great shopping experience.

Asif iqbalDubai, 1 January 2023

★★★★★

Highly recommend others to shop for car insurance plans via Policybazaar.My TPL insurance is about to expire in another month and to continue driving the car I needed to renew the plan. Thanks to Policybazaar's insurance plan option, I managed to purchase a suitable plan. The aftersales service were an icing on the cake. Highly recommend others to shop for car insurance plans via Policybazaar UAE.

More From Car Insurance

- Recent Articles

- Popular Articles

Last Updated : 15 Apr 2026Japanese Car Insurance - Buy Insurance for Japanese Cars in UAEBuy or renew Japanese car insurance in the UAE with Policybazaar.ae. Compare comprehensive & third-party plans, get instant quotes, and enjoy a fast, 100% online purchase of motor insurance for all Japanese cars.

Last Updated : 15 Apr 2026Japanese Car Insurance - Buy Insurance for Japanese Cars in UAEBuy or renew Japanese car insurance in the UAE with Policybazaar.ae. Compare comprehensive & third-party plans, get instant quotes, and enjoy a fast, 100% online purchase of motor insurance for all Japanese cars. Last Updated : 10 Apr 2026Sharjah New EV Charging Laws 2026 - Charges, Penalty, & moreAs the UAE continues to move towards electric mobility, Sharjah has brought new regulations for EV infrastructure. It lays down standard rates, clear charging rules, penalties for improper use, and more.

Last Updated : 10 Apr 2026Sharjah New EV Charging Laws 2026 - Charges, Penalty, & moreAs the UAE continues to move towards electric mobility, Sharjah has brought new regulations for EV infrastructure. It lays down standard rates, clear charging rules, penalties for improper use, and more. Last Updated : 08 Apr 2026Sheikh Rashid Tower Parking in Dubai - Location, Fees, Metro & Access GuideVisiting DWTC? Know about Sheikh Rashid Tower Car Park location, accessibility, nearby venues, and parking convenience for events and exhibitions.

Last Updated : 08 Apr 2026Sheikh Rashid Tower Parking in Dubai - Location, Fees, Metro & Access GuideVisiting DWTC? Know about Sheikh Rashid Tower Car Park location, accessibility, nearby venues, and parking convenience for events and exhibitions. Last Updated : 10 Apr 2026Global Village Car Parking : Free, Premium, VIP & P1–P5 Parking GuideGlobal Village parking guide covering free zones, Premium and VIP parking, walking distance, charges, and mobile app features for a smooth visit.

Last Updated : 10 Apr 2026Global Village Car Parking : Free, Premium, VIP & P1–P5 Parking GuideGlobal Village parking guide covering free zones, Premium and VIP parking, walking distance, charges, and mobile app features for a smooth visit. Last Updated : 08 Apr 2026Dubai Mall Car Parking Guide : Parking Zone, Free Hours, & FeesDubai Mall Car Parking offers free and paid parking. Know parking zones, free hours, & paid parking charges. Also know which car parking should you choose?

Last Updated : 08 Apr 2026Dubai Mall Car Parking Guide : Parking Zone, Free Hours, & FeesDubai Mall Car Parking offers free and paid parking. Know parking zones, free hours, & paid parking charges. Also know which car parking should you choose? Last Updated : 08 Apr 2026Al Qudra Cycle Track Car Park in Dubai: Parking, Timings & Contact NumberAl Qudra Cycle Track Car Park in Dubai offers the tracking, car park, route access. Check location details, opening hours, & best time to visit Al Qudra Cycle Track Dubai.

Last Updated : 08 Apr 2026Al Qudra Cycle Track Car Park in Dubai: Parking, Timings & Contact NumberAl Qudra Cycle Track Car Park in Dubai offers the tracking, car park, route access. Check location details, opening hours, & best time to visit Al Qudra Cycle Track Dubai.

Last Updated : 20 Apr 2026How to Check Car Insurance Status Online in UAE - 2026Check Car Insurance Status Online - Checking your vehicle insurance status online in UAE with these methods RTA Website , EVG , MoI ,Policybazaar.ae & more.

Last Updated : 20 Apr 2026How to Check Car Insurance Status Online in UAE - 2026Check Car Insurance Status Online - Checking your vehicle insurance status online in UAE with these methods RTA Website , EVG , MoI ,Policybazaar.ae & more.- Last Updated : 20 Apr 202610 Best Car Insurance Companies in Dubai, UAE - 2026Checkout the list of top 10 best car insurance companies in Dubai, UAE with their products & service benefits that they offer so you can choose best as per your needs.

Last Updated : 24 Mar 2026How to Transfer Vehicle Ownership in UAE - Process, Documents, FeesTransfer Car Ownership in UAE - Checkout Step by step guidance to transfer your car registration & ownership when you are selling or buy used cars in UAE

Last Updated : 24 Mar 2026How to Transfer Vehicle Ownership in UAE - Process, Documents, FeesTransfer Car Ownership in UAE - Checkout Step by step guidance to transfer your car registration & ownership when you are selling or buy used cars in UAE Last Updated : 20 Apr 2026Abu Dhabi Traffic Fines List 2026 - How to Check & Pay FinesAbu Dhabi Traffic Fines - Get the updated list of Abu Dhabi traffic fines in Abu Dhabi 2026 like - Speed Fines, Car Licence Plates, Reckless Driving Fines, & more. And also know to check and pay Abu Dhabi Police traffic fines.

Last Updated : 20 Apr 2026Abu Dhabi Traffic Fines List 2026 - How to Check & Pay FinesAbu Dhabi Traffic Fines - Get the updated list of Abu Dhabi traffic fines in Abu Dhabi 2026 like - Speed Fines, Car Licence Plates, Reckless Driving Fines, & more. And also know to check and pay Abu Dhabi Police traffic fines. Last Updated : 20 Apr 2026How to Check Black Points on License in Dubai | Black Points DubaiBlack Points Dubai - Know black points system in Dubai & Also know how to check & reduce black points in Dubai, penalty, rule & regulation & more.

Last Updated : 20 Apr 2026How to Check Black Points on License in Dubai | Black Points DubaiBlack Points Dubai - Know black points system in Dubai & Also know how to check & reduce black points in Dubai, penalty, rule & regulation & more..jpg) Last Updated : 21 Apr 2026Abu Dhabi Parking SMS - Format, Codes, Types, Charges, How to PayGet the Comprehensive Guidance for SMS Parking in Abu Dhabi. Also know how to Pay for MAWAQIF Parking, Parking types and charges, Code List, Benefits, Extensions, & more about Abu Dhabi Parking SMS.

Last Updated : 21 Apr 2026Abu Dhabi Parking SMS - Format, Codes, Types, Charges, How to PayGet the Comprehensive Guidance for SMS Parking in Abu Dhabi. Also know how to Pay for MAWAQIF Parking, Parking types and charges, Code List, Benefits, Extensions, & more about Abu Dhabi Parking SMS.

Disclaimer▼