.webp)

- Car Insurance Cost Estimator UAE

- What is Car Insurance Premium?

- Details Required for Calculating Car Insurance Cost

- How Can I Calculate My Car Insurance Premium?

- Benefits of Car Insurance Estimate Calculator in UAE

- Factor Affecting Car Insurance Premium

- How to Reduce Car Insurance Premium in UAE?

- Guide of Car Insurance Dubai

- Car Insurance Renewal Premium

Car Insurance Calculator UAE

Calculate Your Car Insurance Premium Online

Get 12 Free Car Washes

Search Your Car's brand

Nissan

Toyota

Honda

Mitsubishi

Ford

Hyundai

4.7/5

43,419

Central Bank UAE Registration No.: - 123

35+

Insurance Partners

2 Million+

Trusted Customers

1 Million+

Policies Sold

Best Car Insurance in UAE

Some of the best and the cheapest car insurance quotes in Dubai are:

*Above mentioned prices are for Honda City EX 1.5L, 2022 model.

Table of Content

Our car insurance calculator is an online tool that can be used to get an estimate of your car insurance premium. It uses important factors that influence the premium of a car insurance plan such as car brand, make, model, etc. Policybazaar UAE car insurance calculator is a simple and efficient online calculation tool you can use to get a fair idea of your new car insurance premium. You can follow the following steps to use the Policybazaar UAE car insurance premium calculator in the most efficient manner:

- Step1- Enter the brand name, year of manufacture, model of the car and the variant.

- Step2- Once these details are entered, your premium will be calculated automatically. It appears in the bottom-left corner of the calculator.

- Step3- If you change any details entered in the calculator, the premium is updated accordingly. You can enter different brands, variants etc. to see the fluctuation in premium.

- Step4- If you like, you can also proceed directly to view suitable car insurance plans for the car and the variant you have entered in the car insurance premium calculator. Simply click on the “view plans” button to go to our plans’ page.

Details Required for Calculating Car Insurance Cost

Given below is the complete list of details you will need to calculate your car insurance premium using the Policybazaar UAE car insurance calculator:

- Make and model of your car

- The ex-showroom price of the car

- The emirate you reside in

- The year you bought your car

- Whether you made any claims last year

How Can I Calculate My Car Insurance Premium?

A few factors are used in calculating the premium rates of car insurances prices in the UAE. These factors can include – insured declared value of the car, no claim bonus, and price of add-ons. Insured declared value is calculated by subtracting depreciation from the ex-showroom price of the car. IDV can be calculated using an IDV calculator as well. The Premium amount of your car insurance will have further two parts – third-party liability premium and own damage insurance premium.

Car Insurance Premium = (IDV x premium rates + add-on rates) – (no claim bonus + promotional discounts).

The resulting amount is then added with the base price of third-party liability premium to get the final premium amount of your insurance plan. You do not need a third-party car insurance premium calculator here the price is generally fixed and added to the formula automatically.

Premium rates for own damage premiums generally range around 2-3% of the total insured declared value of the car. This is why premium rates are highly affected by the change that occurs in the insured declared value of a vehicle. Depreciation causes a change in the insured declared value of the car which can be calculated using a car insurance depreciation calculator. Further changes occur by considering the secondary elements that affect car insurance premium calculations. You skip all these hefty calculations and get your car insurance premiums calculated using the Policybazaar UAE car insurance estimator. This car insurance EMI calculator will not give you a fair premium rate but also suggest suitable plans for your car.

Benefits of Car Insurance Estimate Calculator in UAE

Several kinds of benefits can come out of calculating your car insurance plans beforehand. Given below are some of the top ones:

- Priority Peek into Insurance Plans: Using a car insurance premium calculator tool to find the premium rates for your car gives you prior insights into the potential plans and prices that will suit you. This makes the overall procedure of finding and choosing plans easier and more swift for you and makes sure that you do not fall for fraudulent schemes.

- Helps in Planning Ahead: Knowing how much maintenance of your car will cost including insurance helps you make a better decision. You can create your budget more efficiently and plan for other factors accordingly as well. Handling your finances smartly is what it’s all about at the end and a car insurance calculator helps a lot in this.

- Gives You a Fair Idea of the Market Trends: Knowing market trends is the first thing you should do whenever buying something or investing. The same applies to car insurance plans as well. Using a car insurance premium calculator will help you in identifying the current estimated insurance rates for your car.

- Helps Understanding How Variable Work: Once you find the basic rate of the car insurance plan for your car using a car insurance calculator, it is easy to understand how a particular variable changes it later. For example, the premium rate will change if you include an add-on on top of the basic plan or if your driving record is not very good. These changes in premium rates are easily identifiable once you have an idea of the base price of the plan.

- Better Comparison Scope: needless to say, knowing the base price for your car insurance plan via a car insurance calculator helps in comparing the available plans and their cost-effectiveness. The better comparison you can draw, the easier it is to choose the perfect plan for your car.

Car Insurance Addons

How to Reduce Car Insurance Premium in UAE?

Maintain a Good Driving Record: As explained before, a good driving record will earn you significant discounts on your car insurance premium.

File Lesser Claims: Avoid filing small claims that can be handled on your own. Instead, save your claims and try to accumulate no claim bonus to get higher discounts on car insurance premium rates.

Avoid Unnecessary Modifications: Aesthetic and performance-enhancing modifications generally increase the premium rates. Modifications increase the maintenance and repair cost of the car which is why the premium goes higher. Some insurance companies do not insure cars with too many modifications. If you like, stick to practical modifications such as anti-theft devices.

Take Higher Deductibles: Deductible is the amount you, the policyholder, is liable to pay out of the total claim amount. A higher deductible amount reduces liability for insurance providers. This is why premium rates come down when deductibles are higher in a car insurance plan.

Accumulate No Claim Bonus: If accumulated ideally, no claim bonus can help reduce your car insurance premium up to 50% in most cases. In some special scenarios, this percentage can even go up to 60-65%. The best way to have your car insurance(تأمين السيارات) premium reduced is by accumulating your no claim bonus and transferring it to the next you buy every time. The car insurance premium calculator also considers NCB when calculating your base premium. So, always keep a track of your NCB.

Avoid Making Small Claims: Making even the smallest claim, except for third party claims, will not only go on your permanent record but also reduce your no claim bonus to nothing. Instead of filing claims for every small repair you get done on your car, try and save it for the big ones. Having a claim history ridden with several claims can jack up your premium while a cleaner one will bring the rates down.

Always Renew on Time: There is a higher chance for your premium rates to rise if you have to re-activate an expired policy or buy a new one from scratch. On top of that, you lose your no claim bonus if an expired policy is not renewed in the next 90 days. Make it a priority to renew your car insurance on time every year.

Shop Online: Finding special promotional discounts on car insurance plans, or any other kind of general insurance, is very rare. But this does not mean you can never get any kind of relaxation on your premium prices. Shopping for your car insurance plans online is the best way to score some discount on top of the no claim bonus. Almost all providers in the UAE offer special online shopping discounts for plans bought online. Check out the latest trend for online shopping discounts.

Guide of Car Insurance Dubai |

|||

|---|---|---|---|

| Engine Damage and Auto Insurance Cover Guide | Guide to Renew Car Registration in Dubai |

Car insurance Cover if my Friend is Driving my Vehicle in Dubai Guide |

|

Car Insurance Renewal Premium

Chances are that your premium rates will remain the same for at least the next three years after buying the car initially. But after that, there can be a change in the premium rates depending on depreciation of the car, condition of the car, insured declared value etc. You can use a car insurance premium calculator to get a fair idea of the changed premium prices. Car insurance premiums for older cars may decrease since the IDV is lower. But it’s best to not choose your insurance plan solely based on premium rates. Consider the extent of coverage you need and then choose the best possible option which is also cost-effective

Veli kaplanAbu Dhabi, 27 May 2026

★★★★★

Quite Affordable Car Insurance in the UAEPolicybazaar.ae was the place where I found the cheapest car insurance in UAE, but without any compromise on what I wanted in coverage. Got a solid comprehensive plan and the difference this time was I thoroughly informed by the team, so chose only the necessary add-ons and saved on costs.

Shyla beeviDubai, 23 May 2026

★★★★★

Hands Down the Best Place for Motor Insurance in the UAEI'd heard of PB.ae from a colleague and decided to try out for car insurance this time. Turns out, this was the best decision with how easy the whole journey was. Never did I ever expect to find the best policies with this much clarity, and that too with detailed explanations. Best site, delivered a 10/10 experience.

Laura Anne HaigDubai, 11 May 2026

★★★★★

Sound Advice on Car InsuranceCredits to Policybazaar.ae for getting me the best car insurance in UAE. The website was great as I could see the top plans, prices and whatnot, but the team was outstanding too. They took time and understood my requirements without rush. This zero pressure thing worked with me, like I actually made an informed choice!

Salma ElgerbyDubai, 5 May 2026

★★★★★

Helpful Experts and Clear Car Insurance OptionsPB people made it easier for me to understand car insurance plans in Dubai. The experts explained the important points in simple language and helped me compare the available options. I could check the premium, coverage and benefits before deciding. The experience was good and I did not feel pushed into buying something I did not need. So YESSSSSS!!!

YasirDubai, 28 April 2026

★★★★★

Expert Advice Made Car Insurance EasierI was not sure which car insurance in the UAE would be right for me. The expert advice from Policybazaar.ae really helped. Instead of just looking at the premium, I understood what coverage I should check, what add-ons may be useful and what things I should avoid. It made me feel more confident before buying the insrance.

Lino JohnDubai, 19 April 2026

★★★★★

Good Platform for Comprehensive Insurance in DubaiI wanted comprehensive car insurance in Dubai and was not sure which plan would offer the right coverage. Policybazaar.ae showed multiple options from different insurers, which helped me compare prices and benefits easily. I liked that I could see important details like coverage, add-ons and claim support before making a decision. It felt more transparent than choosing a plan blindly.

More From Car Insurance

- Recent Articles

- Popular Articles

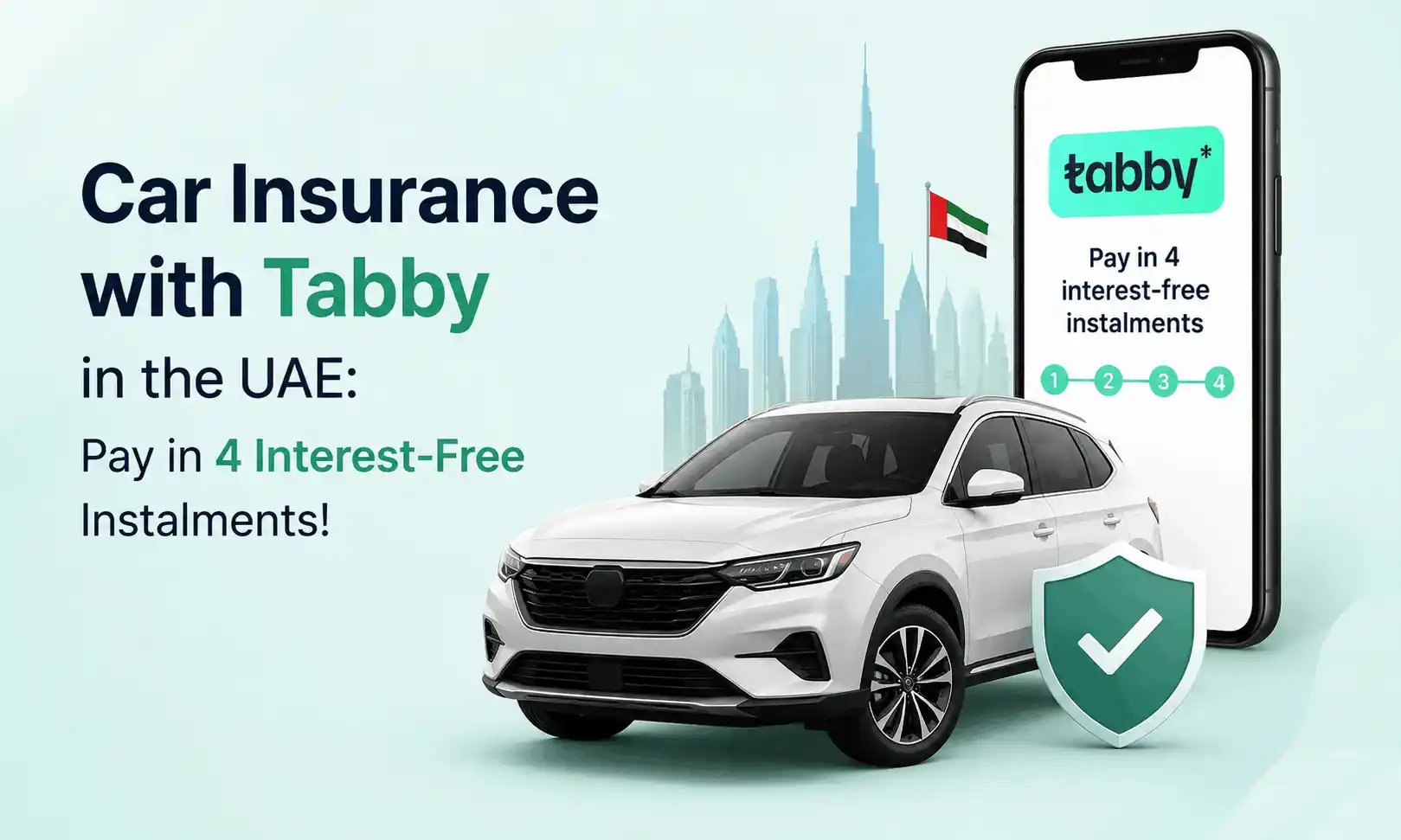

Last Updated : 05 Aug 2026Car Insurance with Tabby in the UAE | Interest-Free PaymentsBuy car insurance with Tabby in the UAE and split your premium into 4 interest-free instalments with no processing fees and no minimum premium requirement.

Last Updated : 05 Aug 2026Car Insurance with Tabby in the UAE | Interest-Free PaymentsBuy car insurance with Tabby in the UAE and split your premium into 4 interest-free instalments with no processing fees and no minimum premium requirement. Last Updated : 04 Aug 2026 Import JDM & Right-Hand-Drive Classic Cars to UAEPlanning to import a JDM or right-hand-drive classic car to the UAE? Explore 2026 import regulations, RTA inspections, import costs, & insurance requirements..

Last Updated : 04 Aug 2026 Import JDM & Right-Hand-Drive Classic Cars to UAEPlanning to import a JDM or right-hand-drive classic car to the UAE? Explore 2026 import regulations, RTA inspections, import costs, & insurance requirements.. Last Updated : 03 Aug 2026Driving to Oman or Saudi Arabia: Which Car Insurance and Border Documents Do You Really Need?Planning to drive from the UAE to Oman or Saudi Arabia? know which car insurance, border permits, and essential documents you need for a smooth cross-border journey.

Last Updated : 03 Aug 2026Driving to Oman or Saudi Arabia: Which Car Insurance and Border Documents Do You Really Need?Planning to drive from the UAE to Oman or Saudi Arabia? know which car insurance, border permits, and essential documents you need for a smooth cross-border journey. Last Updated : 28 Jul 2026Orphaned Chinese Car Brands in the UAE: Insurance and Spare Parts AvailabilityUnderstand what an orphaned car brand is, why some Chinese car brands have exited the UAE market, and how it can affect insurance, repairs, spare parts, and long-term ownership.

Last Updated : 28 Jul 2026Orphaned Chinese Car Brands in the UAE: Insurance and Spare Parts AvailabilityUnderstand what an orphaned car brand is, why some Chinese car brands have exited the UAE market, and how it can affect insurance, repairs, spare parts, and long-term ownership. Last Updated : 28 Jul 2026Smart Summon & Autonomous Parking Accidents in the UAE: Liability ExplainedFind out how liability is determined when a Smart Summon or autonomous parking feature causes an accident in the UAE, and what it means for your car insurance claim.

Last Updated : 28 Jul 2026Smart Summon & Autonomous Parking Accidents in the UAE: Liability ExplainedFind out how liability is determined when a Smart Summon or autonomous parking feature causes an accident in the UAE, and what it means for your car insurance claim. Last Updated : 27 Jul 2026EV Water Damage Insurance in UAE | Flood & Water Ingress Claims GuideKnow how UAE car insurance covers EV water ingress claims after heavy rain. Find out if electric vehicle battery, motor, and flood damage are covered, how to file a claim, and when an EV may be declared a total loss.

Last Updated : 27 Jul 2026EV Water Damage Insurance in UAE | Flood & Water Ingress Claims GuideKnow how UAE car insurance covers EV water ingress claims after heavy rain. Find out if electric vehicle battery, motor, and flood damage are covered, how to file a claim, and when an EV may be declared a total loss.

Last Updated : 04 Jun 2026How to Check Car Insurance Status Online in UAE - 2026Check Car Insurance Status Online - Checking your vehicle insurance status online in UAE with these methods RTA Website , EVG , MoI ,Policybazaar.ae & more.

Last Updated : 04 Jun 2026How to Check Car Insurance Status Online in UAE - 2026Check Car Insurance Status Online - Checking your vehicle insurance status online in UAE with these methods RTA Website , EVG , MoI ,Policybazaar.ae & more.- Last Updated : 31 Jul 202610 Best Car Insurance Companies in Dubai, UAE - 2026Checkout the list of top 10 best car insurance companies in Dubai, UAE with their products & service benefits that they offer so you can choose best as per your needs.

Last Updated : 24 Mar 2026How to Transfer Vehicle Ownership in UAE - Process, Documents, FeesTransfer Car Ownership in UAE - Checkout Step by step guidance to transfer your car registration & ownership when you are selling or buy used cars in UAE

Last Updated : 24 Mar 2026How to Transfer Vehicle Ownership in UAE - Process, Documents, FeesTransfer Car Ownership in UAE - Checkout Step by step guidance to transfer your car registration & ownership when you are selling or buy used cars in UAE Last Updated : 21 Jul 2026Abu Dhabi Traffic Fines 2026 - Complete List, Payment & MoreGet the updated list of Abu Dhabi traffic fines for 2026, including speeding fines, number plate violations, reckless driving penalties, and more. how to check and pay Abu Dhabi Police traffic fines online.

Last Updated : 21 Jul 2026Abu Dhabi Traffic Fines 2026 - Complete List, Payment & MoreGet the updated list of Abu Dhabi traffic fines for 2026, including speeding fines, number plate violations, reckless driving penalties, and more. how to check and pay Abu Dhabi Police traffic fines online..jpg) Last Updated : 15 Jun 2026Abu Dhabi Parking SMS - Format, Codes, Types, Charges, How to PayGet the Comprehensive Guidance for SMS Parking in Abu Dhabi. Also know how to Pay for MAWAQIF Parking, Parking types and charges, Code List, Benefits, Extensions, & more about Abu Dhabi Parking SMS.

Last Updated : 15 Jun 2026Abu Dhabi Parking SMS - Format, Codes, Types, Charges, How to PayGet the Comprehensive Guidance for SMS Parking in Abu Dhabi. Also know how to Pay for MAWAQIF Parking, Parking types and charges, Code List, Benefits, Extensions, & more about Abu Dhabi Parking SMS. Last Updated : 01 May 2026How to Check Black Points on License in Dubai | Black Points DubaiBlack Points Dubai - Know black points system in Dubai & Also know how to check & reduce black points in Dubai, penalty, rule & regulation & more.

Last Updated : 01 May 2026How to Check Black Points on License in Dubai | Black Points DubaiBlack Points Dubai - Know black points system in Dubai & Also know how to check & reduce black points in Dubai, penalty, rule & regulation & more.

Disclaimer▼