As individuals, we always strive to protect our families and loved ones and secure their futures. Health, a pivotal aspect of life, is one of the keys to securing your loved ones' future. Despite our numerous steps to ensure a wholesome and well-rounded existence, unforeseen health emergencies and accidents can take us by surprise. In such adverse situations, having the right health insurance can prove to be the ultimate saviour.

While purchasing health insurance for a family may appear straightforward, it is essential to keep a few factors in mind to ensure that the policy is comprehensive and sufficient to meet your family’s requirements.

In the article below, we will discuss some key factors to keep in mind when purchasing a health insurance policy for our families. Let’s start without further ado -

1. Conduct Thorough Market Research

In the UAE, there are various types of health insurance policies available tailored to meet the needs of different age groups, life stages, and the propensity for health issues. For this reason, conducting thorough market research before opting for a plan is vital.

The first and foremost step here is to comprehend which type of plan best meets your and your family member's requirements to make a well-informed decision.

For instance –

Individual health insurance plans cover an individual and are suitable for single individuals or those without dependents.

You can go for family floater plans to cover your entire family including spouses, children, and parents. The standard benefit of a family floater plan is that it offers comprehensive coverage for medical expenses incurred by any member of the family.

Another option is a senior citizen health insurance plan which is specifically designed for senior citizens and provides coverage for age-related illnesses and medical conditions.

In order to get assistance while making a choice, you can always contact our in-house health insurance expert team and pick the right health insurance policy for your family.

2. Sum Insured and Premium

When choosing a health insurance policy for a family, it is vital to consider the sum insured and the premium amount. The former refers to the maximum amount that the insurance company will pay for the medical expenses in case of hospitalisation.

A higher sum insured implies that you are better protected against any unexpected medical expenses. However, while a lower sum insured may save you money on premiums, it could leave you and your family underinsured in case of a major medical event.

The premium, on the other hand, is the amount that you have to pay to the insurance company on a regular basis in exchange for coverage. Choosing the premium amount that you can afford to pay consistently over the long term is advisable. Missing premium payments can lead to the termination of your policy or denial of coverage.

Simply put, it is essential to strike a balance between the sum insured and the premium amount when opting for a health insurance policy for a family. You should opt for adequate coverage at a price that you can afford.

3. Limits and Sub-Limits of Health Insurance Policy

Another factor that impacts your choice of health insurance policy for the family is the limits and sub-limits of the plan. Limits refer to the maximum amount that the concerned insurance company will pay for a specific type of treatment coverage like room rent, ambulance charges, or any other surgical procedures.

The sub-limits of a health insurance plan, on the other hand, refer to the maximum amount that the insurance provider will pay for a specific aspect of a medical expense, which can include fees for diagnostic tests, ICU charges, medical facility fees, and more.

By understanding the limits and sub-limits, you can decide which health insurance is ideal for your family. Choosing a health insurance policy for a family with reasonable limits and sub-limits is advisable to provide sufficient coverage for your family's medical requirements.

For example, if you have a low room rent limit, you would have to pay a considerable amount out of your pocket if you require a higher-priced room in the hospital. Similarly, if the sub-limit of doctor's fees is low, you have to bear the additional amount out of your pocket.

4. Network List

A network list includes hospitals, doctors, and medical facilities contracted with the insurance provider to provide cashless medical facilities to insured individuals. If you choose a healthcare provider not listed in your network list, you may have to pay out of pocket first before applying for the reimbursement claim.

It is highly recommended to check whether the healthcare providers that you prefer are part of the network list. By reviewing the network list of your health insurance policy, you can ensure that your family has access to quality healthcare providers in your area. Another factor while opting for the health insurance policy for the family is to consider the availability of hospitals and clinics near your residence, the expertise and reputation of doctors in the network, and the range of covered medical services.

You can get the list of a network of hospitals on our health insurance quotes page. For this, you just need to visit the official website of Policybazaar UAE, head to the 'health insurance' page, fill out the lead form, and submit it. You will be redirected to the 'health insurance quotes' page, where you can explore various health insurance plans from the top insurers. Click on the 'network list' link adjacent to the plan and see the network hospitals available with the plan.

5. Claim Process

The claim process refers to the steps that have to be followed to request reimbursement from the insurance company for the medical expenses that are covered by the policy. While you can avail of the cashless medical facility if you get treated in the network hospital, you would need to pay medical expenses out of your pocket and then apply for the reimbursement medical insurance claim if you opt for treatment in a non-network hospital.

Before choosing a health insurance policy for your family, it is essential to understand the claim process, as it can affect how quickly and efficiently you receive reimbursement for medical expenses.

Apart from a simple, transparent health insurance claim, it is also important to be aware of the documentation required to make a claim, the period within which you need to make a claim, and the entire process. A good health insurance policy for a family must have a streamlined and efficient claim process that would make it easy for you to access the benefits of the policy.

Furthermore, you should look for an insurance provider which has a dedicated customer service team that can assist you with any questions or issues related to the claim process and have a user-friendly online portal or mobile application to help you to track the status of your claim application.

This is the period during which you are not eligible to receive coverage for specific medical conditions or treatments. It is crucial to be aware of the waiting period of your health insurance policy as it can affect your ability to access medical treatment when you need it most.

For instance, if your family member has a pre-existing medical condition subject to a waiting period, you may have to wait for a defined period before you can receive coverage for that disease.

Keeping in mind the waiting period of your health insurance policy, you can look for health insurance policies for the family that have shorter waiting periods or waive the waiting period for specific medical conditions.

7. Opt for Coverage Riders

Coverage riders or add-ons enhance your standard basic health insurance policy, ensuring that your family can access a wider range of medical services at nominal additional costs. Multiple coverage riders are available that can cater to the unique healthcare needs of your family like critical illness rider, which provides coverage for medical expenses related to critical illnesses such as heart attacks and more.

By opting for coverage riders, you can tailor your health insurance policy to your family's specific healthcare needs and ensure that you have adequate coverage for unexpected medical expenses. You should carefully review the available riders and consider factors such as your family's medical history, lifestyle, and budget before selecting a rider.

Note that with the addition of a rider, the premium of your health insurance policy would generally increase. Thus, you should also consider the premium cost of the coverage riders and how it will affect the overall cost of your health insurance policy for your family.

8. Exclusions List

Another thing that you must check in your health insurance policy for your family is the exclusion list, as it can significantly impact your coverage and out-of-pocket expenses. Exclusions simply refer to the treatments or services that your insurance provider will not cover.

If you or your family members require treatment for a condition that falls under the exclusion list, you shall be responsible for the medical expenses. For example, if your health insurance policy excludes pre-existing conditions and one of your family members has a chronic illness, you may not be able to claim any expenses related to the treatment.

Thus, it is of the utmost importance to look for exclusions in your health insurance policy, as it will help you select a plan that provides comprehensive coverage for your family’s requirements and avoid any unexpected financial burdens.

9. Value-Added Benefits in your Health Insurance Policy

Value-added benefits in your health insurance policy provide additional services or coverages that can enhance your family's overall health and well-being. Some common value-added benefits include free-health check-ups, free doctor's consultations, assessment of your health, and more.

By considering these value-added benefits, you can ensure that your family has access to myriad benefits that can help you save on healthcare costs in the long run. For this reason, it is recommended to buy health insurance for a family with value-added benefits that complement your family's healthcare needs.

10. Co-payment, Coinsurance, and Deductible

Co-payment, coinsurance, and deductible are the three important terms that must necessarily be understood when it comes to picking a health insurance policy for your family.

The copayment is the amount that you are required to pay as your share for the treatment, with the remaining amount to be covered by the insurance policy. For instance, if you have a 20% co-payment for a medical procedure that costs AED 1,000, you will pay AED 200 while your insurance provider will cover the remaining amount of AED 800.

Deductible refers to the amount of money that you are responsible for paying before your insurance provider begins covering the costs of your medical expenses. Again, if you have, say, an AED 1000 deductible, you will need to pay AED 1,000 out of pocket for your medical expenses before your insurance provider begins covering the costs. Once you have met your deductible, your insurance provider will typically cover a portion of your medical expenses through copayments or coinsurance.

Yet another key term is coinsurance, which refers to the fixed percentage cost that you are required to bear after settling the deductible amount. Let’s assume that your total medical expenses are AED 20,000 and the deductible is AED 5,000. After paying the deductible amount, suppose, you may need to pay 10% of AED 15,000 as coinsurance which is AED 15,000 as per the coinsurance clause of your health insurance policy. The remaining amount of AED 13,500 shall be paid by the insurance company.

Wrapping Up

Choosing a health insurance policy for the family requires careful consideration and research. You would need to understand the coverage options, benefits, exclusions, and cost-sharing arrangements of each policy you are considering. You should also evaluate your family's healthcare needs, budget, and preferences to select a policy that meets your requirements.

Other factors to consider include network coverage, value-added benefits, and customer service. By taking the time to thoroughly review and compare policies, you can make an informed decision and select the best health insurance plan for your family's health and financial well-being.

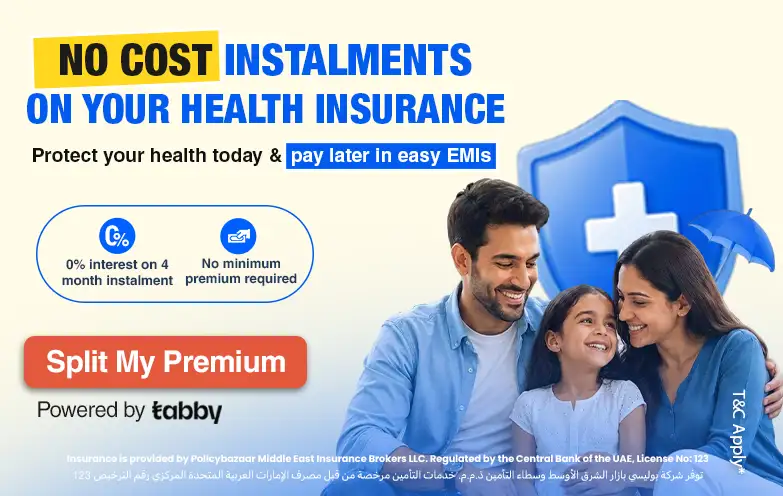

Last Updated : 17 Jun 2026Buy Insurance in Installments UAE | 0% Interest via TabbySplit your health or car insurance premium into 4 monthly payments at 0% interest with Tabby. No minimum premium. Coverage starts day one. Available at Policybazaar.ae.

Last Updated : 09 Jun 2026How to Boost Immunity in Children Naturally | UAEBoost your child's immunity naturally with proper sleep, balanced diet, daily exercise, and timely vaccinations - no supplements needed in most cases.

Last Updated : 09 Jun 2026Digital Detox: Why Your Brain Needs a Break from ScreensDigital detox is a regular break from screens that reduces stress, improves sleep quality, and boosts productivity. Learn the signs you need one and how to start.

Last Updated : 08 Jun 2026PCOS Officially Renamed PMOS – What It Means for WomenPCOS is now officially PMOS – Polyendocrine Metabolic Ovarian Syndrome. Learn what this landmark 2026 name change means for 170 million women worldwide.

Last Updated : 03 Jun 202620-Minute Workouts for Busy Professionals | Stay Fit Fast4 proven 20-minute workout routines for busy professionals. HIIT, strength, office-friendly & fat-burning cardio — stay fit without long gym sessions.

Last Updated : 03 Jun 2026Plant-Based Diet: Complete Guide to Benefits & FoodsA plant-based diet boosts heart health, weight loss, and immunity. Explore benefits, 5 food groups, and tips to get started in the UAE.

Last Updated : 10 Feb 2026How to Check Medical Insurance Status with Emirates ID?Emiratis will now be able to use their Emirates ID cards not only to go through immigration gates at the airport but to avail of medical services in the UAE.

Last Updated : 16 Jun 2026Best Health Insurance Companies in Dubai, UAE 2026Find the Top 10+ Health Insurance Companies in Dubai, UAE Offering Comprehensive Health Insurance Coverage and Exceptional Services at Affordable Prices.

Last Updated : 26 May 2026How to Check the Status of Your Health Insurance Online?The easiest way to get familiar with your plan details or check the active status is to do it online. Let’s figure out how to check if your health insurance plan is active online.

Last Updated : 08 Jan 2026Dental Insurance UAE: Dental Insurance Types, Coverage & BenefitsDental Insurance UAE: Know All about Dental Insurance, Types, Coverage & Benefits. Dental Insurance Covering Most of the Dental Treatments, You can Drop off Your Worries About Costly Therapies.

Last Updated : 11 Feb 2026Can You Buy Health Insurance for New Born Baby in UAE?Don't know whether you can buy medical insurance for new born baby in UAE? In this article we’ll share everything you need to know about health insurance for newborn baby.

Last Updated : 27 Nov 2025Where Can I Get Medical Help Without Having Health Insurance in UAE?Not everyone in the UAE can afford to buy a health insurance policy to avail of quality medical care benefits. To help out such people, we have listed here a few places and ways of getting medical help.

.png)

Last Updated : 17 Jun 2026Buy Insurance in Installments UAE | 0% Interest via TabbySplit your health or car insurance premium into 4 monthly payments at 0% interest with Tabby. No minimum premium. Coverage starts day one. Available at Policybazaar.ae.

Last Updated : 17 Jun 2026Buy Insurance in Installments UAE | 0% Interest via TabbySplit your health or car insurance premium into 4 monthly payments at 0% interest with Tabby. No minimum premium. Coverage starts day one. Available at Policybazaar.ae. Last Updated : 09 Jun 2026How to Boost Immunity in Children Naturally | UAEBoost your child's immunity naturally with proper sleep, balanced diet, daily exercise, and timely vaccinations - no supplements needed in most cases.

Last Updated : 09 Jun 2026How to Boost Immunity in Children Naturally | UAEBoost your child's immunity naturally with proper sleep, balanced diet, daily exercise, and timely vaccinations - no supplements needed in most cases. Last Updated : 09 Jun 2026Digital Detox: Why Your Brain Needs a Break from ScreensDigital detox is a regular break from screens that reduces stress, improves sleep quality, and boosts productivity. Learn the signs you need one and how to start.

Last Updated : 09 Jun 2026Digital Detox: Why Your Brain Needs a Break from ScreensDigital detox is a regular break from screens that reduces stress, improves sleep quality, and boosts productivity. Learn the signs you need one and how to start. Last Updated : 08 Jun 2026PCOS Officially Renamed PMOS – What It Means for WomenPCOS is now officially PMOS – Polyendocrine Metabolic Ovarian Syndrome. Learn what this landmark 2026 name change means for 170 million women worldwide.

Last Updated : 08 Jun 2026PCOS Officially Renamed PMOS – What It Means for WomenPCOS is now officially PMOS – Polyendocrine Metabolic Ovarian Syndrome. Learn what this landmark 2026 name change means for 170 million women worldwide.-(2)-(2).webp) Last Updated : 03 Jun 202620-Minute Workouts for Busy Professionals | Stay Fit Fast4 proven 20-minute workout routines for busy professionals. HIIT, strength, office-friendly & fat-burning cardio — stay fit without long gym sessions.

Last Updated : 03 Jun 202620-Minute Workouts for Busy Professionals | Stay Fit Fast4 proven 20-minute workout routines for busy professionals. HIIT, strength, office-friendly & fat-burning cardio — stay fit without long gym sessions.-(2).webp) Last Updated : 03 Jun 2026Plant-Based Diet: Complete Guide to Benefits & FoodsA plant-based diet boosts heart health, weight loss, and immunity. Explore benefits, 5 food groups, and tips to get started in the UAE.

Last Updated : 03 Jun 2026Plant-Based Diet: Complete Guide to Benefits & FoodsA plant-based diet boosts heart health, weight loss, and immunity. Explore benefits, 5 food groups, and tips to get started in the UAE. Last Updated : 10 Feb 2026How to Check Medical Insurance Status with Emirates ID?Emiratis will now be able to use their Emirates ID cards not only to go through immigration gates at the airport but to avail of medical services in the UAE.

Last Updated : 10 Feb 2026How to Check Medical Insurance Status with Emirates ID?Emiratis will now be able to use their Emirates ID cards not only to go through immigration gates at the airport but to avail of medical services in the UAE. Last Updated : 16 Jun 2026Best Health Insurance Companies in Dubai, UAE 2026Find the Top 10+ Health Insurance Companies in Dubai, UAE Offering Comprehensive Health Insurance Coverage and Exceptional Services at Affordable Prices.

Last Updated : 16 Jun 2026Best Health Insurance Companies in Dubai, UAE 2026Find the Top 10+ Health Insurance Companies in Dubai, UAE Offering Comprehensive Health Insurance Coverage and Exceptional Services at Affordable Prices. Last Updated : 26 May 2026How to Check the Status of Your Health Insurance Online?The easiest way to get familiar with your plan details or check the active status is to do it online. Let’s figure out how to check if your health insurance plan is active online.

Last Updated : 26 May 2026How to Check the Status of Your Health Insurance Online?The easiest way to get familiar with your plan details or check the active status is to do it online. Let’s figure out how to check if your health insurance plan is active online. Last Updated : 08 Jan 2026Dental Insurance UAE: Dental Insurance Types, Coverage & BenefitsDental Insurance UAE: Know All about Dental Insurance, Types, Coverage & Benefits. Dental Insurance Covering Most of the Dental Treatments, You can Drop off Your Worries About Costly Therapies.

Last Updated : 08 Jan 2026Dental Insurance UAE: Dental Insurance Types, Coverage & BenefitsDental Insurance UAE: Know All about Dental Insurance, Types, Coverage & Benefits. Dental Insurance Covering Most of the Dental Treatments, You can Drop off Your Worries About Costly Therapies. Last Updated : 11 Feb 2026Can You Buy Health Insurance for New Born Baby in UAE?Don't know whether you can buy medical insurance for new born baby in UAE? In this article we’ll share everything you need to know about health insurance for newborn baby.

Last Updated : 11 Feb 2026Can You Buy Health Insurance for New Born Baby in UAE?Don't know whether you can buy medical insurance for new born baby in UAE? In this article we’ll share everything you need to know about health insurance for newborn baby. Last Updated : 27 Nov 2025Where Can I Get Medical Help Without Having Health Insurance in UAE?Not everyone in the UAE can afford to buy a health insurance policy to avail of quality medical care benefits. To help out such people, we have listed here a few places and ways of getting medical help.

Last Updated : 27 Nov 2025Where Can I Get Medical Help Without Having Health Insurance in UAE?Not everyone in the UAE can afford to buy a health insurance policy to avail of quality medical care benefits. To help out such people, we have listed here a few places and ways of getting medical help.