Life Insurance for Singles in the UAE: Why You Shouldn’t Wait to Get Covered

Many people believe that life insurance is only necessary after marriage or when you have children. As a result, single individuals often delay purchasing a policy, assuming they have no dependents to protect.

35+ Critical Illnesses

Issuance

Coverage

4.6/5

35,368

Insurance Partners

Trusted Customers

Policies Sold

Starting @ AED 50/month*

However, this assumption overlooks an important reality: life insurance is not just about dependents — it’s also about financial security, debt protection, and long-term planning.

For many UAE residents, especially young professionals and entrepreneurs, buying a life policy early can be one of the smartest financial decisions. It helps protect loved ones, manage liabilities, and lock in lower premiums for decades.

This guide explains why life insurance for singles in the UAE matters, how much coverage you may need, and how to choose the right policy

Key Takeaways

- Life insurance for singles can protect family members from financial burdens such as loans or funeral costs

- Buying term life insurance for singles early allows you to lock in lower premiums while you are young and healthy

- Policies can help cover education loans, personal debts, or co-signed liabilities

- Some plans offer wealth-building features and long-term financial planning benefits

- Choosing the right policy depends on your financial goals, liabilities, and future plans

Buy Best Life Insurance Plan in UAE

Some of the best Term Insurance quotes in UAE & Dubai are:

Do Single People Need Life Insurance in the UAE?

Yes, life insurance can still be valuable even if you are unmarried. While you may not currently have a spouse or children, many singles in the UAE still have financial responsibilities such as —

- Supporting ageing parents

- Paying off personal loans or education loans

- Running a business or startup

- Planning for future financial goals

If something unexpected happens, these responsibilities may fall on your family members. Life insurance for singles ensures that your financial obligations are covered, preventing loved ones from facing financial stress.

Why Singles Often Delay Buying Life Insurance?

Despite the benefits, many single individuals postpone purchasing life insurance. The most common reasons include —

1. “I Don’t Have Dependents”

Many singles believe insurance is only for people with families. However, parents, siblings, or co-signers on loans may still depend on you financially.

2. Employer Health Insurance Feels Sufficient

Corporate health insurance is certainly helpful. However, it does not provide life cover or financial protection for your family if you pass away.

3. It Feels Like an Unnecessary Expense

Term life insurance is often viewed as a cost rather than a financial protection strategy.

4. Focus on Other Investments

Many young professionals prioritise investments like stocks, property, or savings. All these options are great. However, insurance complements investments by protecting financial goals.

Should Single People Buy Life Insurance?

Short answer: of course, yes!

At first glance, life insurance for singles may seem unnecessary. However, buying a policy early can provide both protection and financial flexibility as your life evolves.

Here are some of the key advantages —

1. Lower Premiums When You Buy Early

Age and health are two of the biggest factors influencing the cost of life insurance for unmarried individuals. When you purchase a policy while you are young and healthy, insurance companies typically offer significantly lower premiums.

For example, a healthy individual in their late 20s may qualify for affordable coverage that can remain fixed for the duration of the policy. Waiting until your 40s, meanwhile, can often result in substantially higher premiums.

2. Protection Against Debts and Financial Liabilities

Many single individuals in the UAE have financial commitments, such as:

- Education loans

- Personal loans

- Car loans

- Credit card balances

If you have a co-signer on a loan or financial obligations shared with family members, life insurance ensures those debts do not become someone else’s burden. The policy payout can help settle outstanding liabilities quickly.

3. Financial Support for Parents or Dependents

Even if you are unmarried, you may still have people who rely on you financially. This could include —

- Ageing parents

- Younger siblings

- Extended family members

Life insurance for singles provides financial protection to such individuals’ dependents, helping them manage expenses in case something unexpected happens.

4. Building a Financial Asset Over Time

Certain types of life insurance accumulate cash value over time. This means your policy can serve as both —

- Financial protection

- A long-term financial asset

You’re free to use the accumulated value for future goals, be it retirement planning, emergencies, or any large expenses.

How to Choose the Best Life Insurance for Single Adults?

Choosing the best life insurance for single adults requires careful evaluation of your financial situation, goals, and responsibilities.

The following steps can help you make an informed decision —

1. Assess Your Financial Responsibilities

Start by reviewing your current and potential financial obligations. These may include:

- Outstanding loans

- Supporting parents

- Future marriage plans

- Business investments

- Property purchases

2. Define Your Long-Term Financial Goals

Your life policy should align with your broader financial plans. For example, you may want to use life insurance to support —

- Starting a business

- Retirement planning

- Property ownership

- Supporting family members

3. Calculate the Right Coverage Amount

Financial planners often recommend coverage of at least 10–15 times your annual income. However, the exact amount depends on factors such as —

- Existing debts

- Financial support for family members

- Future financial goals

- Expected living costs

4. Choose Useful Policy Riders

Many insurers offer optional add-on benefits (riders) that enhance coverage. Some common riders include —

- Critical illness cover

- Accidental death benefit

- Waiver of premium

- Disability income protection

5. Compare Insurers Carefully

Not all insurers offer the same service quality. When selecting a provider, take a look at —

- Claim settlement ratio

- Financial stability of the insurer

- Customer service reputation

- Policy flexibility

Comparing multiple insurers at Policybazaar.ae to choose a policy that balances your coverage, reliability, and cost.

6. Consult a Financial Advisor

If you are unsure which policy is right for you, speaking with a licensed financial advisor like Policybazaar.ae can help you. An advisor can assist with —

- Calculating the correct coverage amount

- Choosing between term and permanent insurance

- Understanding policy features and riders

What Determines the Cost of Life Insurance for Singles?

Infographic Source: Gemini

The premium for life insurance for unmarried individuals varies as per several factors. Some of the most important ones include:

Age: Younger applicants typically receive lower premiums because they are considered lower risk.

Health Status: Medical history and lifestyle habits can influence the cost of coverage.

Policy Type

- Term life insurance generally has lower premiums

- Whole life or ULIP may cost more due to investment features

Coverage Amount: Higher coverage amounts naturally result in higher premiums.

Policy Duration: Longer policy terms can also influence pricing. Generally, the longer the term, the higher the premium.

Because these factors vary widely, it is important to compare the best life insurance for single adults before making a decision.

How Much Life Insurance Does a Single Person Need?

The ideal coverage amount of term life insurance for singles depends on your financial responsibilities. A simple approach is to estimate —

Step 1: Calculate Outstanding Debts

Include liabilities such as —

- Education loans

- Personal loans

- Credit card balances

- Car loans

Step 2: Consider Financial Support for Family

If you provide financial support to parents or siblings, include the years of living expenses.

Step 3: Add Final Expenses

Funeral and medical expenses can be costly, even in the UAE.

Step 4: Plan for Future Goals

You may want to include funds for —

- Future family plans

- Business investments

- Property purchases

Many financial advisors recommend coverage of at least 5–10 times your annual income.

When Should Singles Review Their Life Insurance Policy?

Your life coverage needs may change as your life evolves. It is a good idea to review your coverage when major life events occur, such as —

- Marriage or partnership

- Buying a home

- Starting a business

- Significant income increase

- Taking on new financial responsibilities

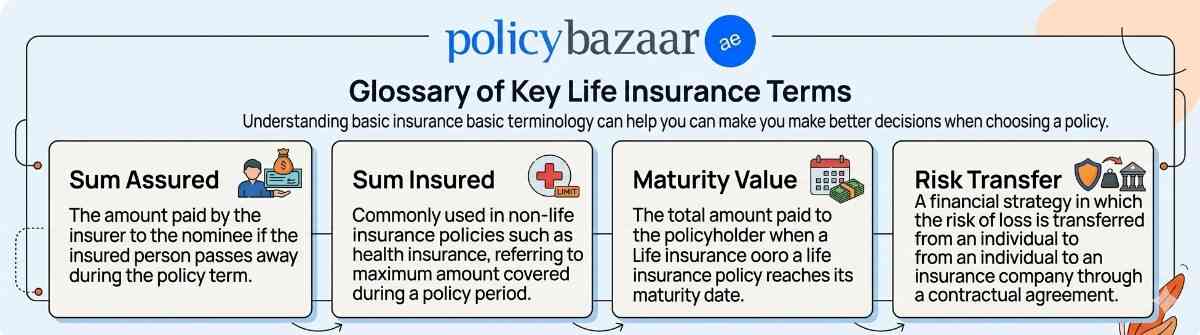

Glossary of Key Life Insurance Terms

Infographic Source: Gemini

Understanding basic insurance terminology can help you make better decisions when choosing a policy.

Sum Assured

The amount paid by the insurer to the nominee if the insured person passes away during the policy term

Sum Insured

Commonly used in non-life insurance policies, such as health insurance, referring to the maximum amount covered during a policy period

Maturity Value

The total amount paid to the policyholder when a life insurance policy reaches its maturity date

Risk Transfer

A financial strategy in which the risk of loss is transferred from an individual to an insurance company through a contractual agreement

Start Planning Your Financial Future Today with Policybazaar.ae

Being single does not mean you should delay financial protection. In fact, life insurance for singles can be one of the smartest financial decisions you make early in life. It protects your loved ones, secures your financial obligations, and helps you plan confidently for the future.

If you are considering a life policy in the UAE, compare your options carefully at Policybazaar.ae, evaluate your financial needs, and choose coverage that supports your long-term goals. Starting early can help you lock in affordable premiums and build a stronger financial future.

Disclaimer: This article is intended for general informational purposes only and does not constitute financial, insurance, or investment advice. Insurance terms, eligibility, coverage, and premiums may vary depending on the insurer and the applicant’s profile. Readers in the UAE should consult a licensed insurance advisor or authorised provider before purchasing any life insurance policy.

FAQs for Life Insurance for Singles

Is life insurance worth it if you’re single?

Yes, life coverage is still important, even if you’re single. It helps cover financial obligations like loans, credit card balances, or funeral expenses. It can also provide financial support to parents or other dependents who rely on you.

When is the best time to buy life insurance for unmarried individuals?

The best time is as early as possible, especially when you are young and healthy. This helps secure lower premiums.

What are the main benefits of life insurance for single people?

Life insurance protects your family from financial burdens by covering outstanding debts or final expenses. It can also help you leave a financial legacy or support a cause or charity that matters to you.

How much life insurance should a single person get?

The right coverage depends on your financial responsibilities, debts, and future goals. Many financial experts suggest choosing coverage equal to 5–10 times your annual income to ensure adequate financial protection.

What type of life insurance is best for singles?

A term life policy is often the most suitable option for singles because it offers affordable coverage for a specific period. Whole or universal life insurance may be useful if you want protection with cash value.

When is the best time to buy life insurance if I’m single?

The best time to buy life insurance for singles is when you are young and healthy. Starting early usually means lower premiums and better coverage options. This helps you lock in affordable protection for the future.

How can Policybazaar.ae help me choose the right plan?

We help you compare term life insurance for singles from leading insurers in the UAE. You can review quotes, understand coverage options, and get expert guidance to choose a policy that fits your needs.

Why is life insurance important for singles?

A life plan helps singles manage financial responsibilities such as loans, final expenses, or supporting ageing parents. It can also support long-term financial planning and provide peace of mind even without immediate dependents.

How much does life insurance cost for single individuals?

Life insurance premiums depend on factors like age, health, lifestyle, and the type of policy chosen. Generally, younger and healthier individuals qualify for lower premiums. Note that term insurance is typically the most affordable option.

What should singles consider before buying life insurance?

Singles should evaluate their financial obligations, long-term goals, and budget before purchasing a policy. Comparing coverage options and consulting a financial advisor can help ensure the policy meets future needs.

Know More About Other Investment Option

Aashima Mongia

More From Term Insurance

- Recent Articles

- Popular Articles

Last Updated : 26 Mar 2026Credit Life Insurance in UAE: Meaning, Benefits, Types & Who Should BuyLearn what credit life insurance is, how it works, and its benefits in UAE. Explore loan protection insurance, types, and best options for personal loans & mortgages.

Last Updated : 26 Mar 2026Credit Life Insurance in UAE: Meaning, Benefits, Types & Who Should BuyLearn what credit life insurance is, how it works, and its benefits in UAE. Explore loan protection insurance, types, and best options for personal loans & mortgages. Last Updated : 19 Mar 2026Digital Life Insurance Plans in UAE: Buy Instant Life Insurance Online & Paperless PolicyExplore digital life insurance plans in the UAE. Learn how digital life insurance works, benefits of buying digital insurance policy, and get instant life insurance online with a paperless process.

Last Updated : 19 Mar 2026Digital Life Insurance Plans in UAE: Buy Instant Life Insurance Online & Paperless PolicyExplore digital life insurance plans in the UAE. Learn how digital life insurance works, benefits of buying digital insurance policy, and get instant life insurance online with a paperless process. Last Updated : 12 Mar 2026How Much Does Life Insurance Cost in UAE? (Monthly Premium Guide 2026Find out how much life insurance costs in the UAE. Compare monthly premiums by age, coverage amount, and policy type to choose the right protection plan.

Last Updated : 12 Mar 2026How Much Does Life Insurance Cost in UAE? (Monthly Premium Guide 2026Find out how much life insurance costs in the UAE. Compare monthly premiums by age, coverage amount, and policy type to choose the right protection plan. Last Updated : 10 Feb 2026Term Insurance Comparison in UAE 2026: Compare Term Life Insurance Plans & RatesCompare term insurance plans in the UAE. Check term life insurance rates, riders, claim settlement ratios, and coverage to choose the right plan for your family.

Last Updated : 10 Feb 2026Term Insurance Comparison in UAE 2026: Compare Term Life Insurance Plans & RatesCompare term insurance plans in the UAE. Check term life insurance rates, riders, claim settlement ratios, and coverage to choose the right plan for your family. Last Updated : 03 Feb 2026Top 10 Life Insurance Companies in India 2026: Best Term & Life Policies ComparedDiscover the top 10 life insurance companies in India. Compare claim settlement ratio, solvency, and the best term & life insurance policies for residents and NRIs.

Last Updated : 03 Feb 2026Top 10 Life Insurance Companies in India 2026: Best Term & Life Policies ComparedDiscover the top 10 life insurance companies in India. Compare claim settlement ratio, solvency, and the best term & life insurance policies for residents and NRIs.

Last Updated : 24 Dec 2025Best Life Insurance Companies in Dubai, UAE (2026 Updated List) Find out more about life insurance companies in the UAE and compare features and benefits offered. Buy best life insurance plan now!

Last Updated : 24 Dec 2025Best Life Insurance Companies in Dubai, UAE (2026 Updated List) Find out more about life insurance companies in the UAE and compare features and benefits offered. Buy best life insurance plan now! Last Updated : 19 Mar 2026Best Self Employed Insurance Plans Online in UAETerm Insurance Plans for Self Employed - Know how to select the best term plan for self-employed individuals & why it is required and who needs it only at Policybazaar.ae

Last Updated : 19 Mar 2026Best Self Employed Insurance Plans Online in UAETerm Insurance Plans for Self Employed - Know how to select the best term plan for self-employed individuals & why it is required and who needs it only at Policybazaar.ae Last Updated : 02 Jan 2026Term Insurance for NRI | Best Term Insurance Plan for NRI in UAETerm Insurance for NRI - Compare and Buy best term insurance policies for NRI in UAE & know important things before buying the term plan for NRI in UAE.

Last Updated : 02 Jan 2026Term Insurance for NRI | Best Term Insurance Plan for NRI in UAETerm Insurance for NRI - Compare and Buy best term insurance policies for NRI in UAE & know important things before buying the term plan for NRI in UAE. Last Updated : 23 Mar 2026Term Insurance for Spouse in UAE - Features & BenefitsTerm Insurance for Spouse - Choose the best term insurance plan for your spouse in UAE with features & Benefits. Also, know who can buy a spouse term insurance plan.

Last Updated : 23 Mar 2026Term Insurance for Spouse in UAE - Features & BenefitsTerm Insurance for Spouse - Choose the best term insurance plan for your spouse in UAE with features & Benefits. Also, know who can buy a spouse term insurance plan. Last Updated : 12 Dec 2025Top Life Insurance Plans for Expats in the UAE: Protect Your Family's FutureDiscover the best life insurance options for expatriates in the UAE. Learn about key benefits, top plans, and essential tips to secure financial protection for your loved ones.

Last Updated : 12 Dec 2025Top Life Insurance Plans for Expats in the UAE: Protect Your Family's FutureDiscover the best life insurance options for expatriates in the UAE. Learn about key benefits, top plans, and essential tips to secure financial protection for your loved ones. Last Updated : 19 Sep 2025Short Term Disability Insurance | Benefits & How It WorksDiscover short term disability insurance options to safeguard your income during challenging times. Get affordable coverage tailored to your needs!

Last Updated : 19 Sep 2025Short Term Disability Insurance | Benefits & How It WorksDiscover short term disability insurance options to safeguard your income during challenging times. Get affordable coverage tailored to your needs!