Premium Lock in Health Insurance: Lock Your Premium for Up to 5 Years

UAE healthcare costs continue to rise every year due to medical inflation and age-based premium hikes. However, your insurance can now save you from premium increases.read more

AED 1 million Health cover starting @4/Day

4.7/5

43,419

Trusted Customers

Insurance Partners

Policies Sold

What is Premium Lock in Health Insurance in the UAE?

Premium Lock is an optional add-on available with Hayah and DIC health insurance plans offered exclusively through Policybazaar.ae and powered by Care Health Insurance.

As the name suggests, this rider allows you to lock your health insurance premiums at the entry-age pricing for up to 5 years. During the period, the premium remains protected from

✅ Annual medical inflation

✅ Age-related premium increase

✅ Standard annual increases upon renewal

Premium Lock in UAE Health Insurance: Key Highlights

|

Type of Rider |

Optional add-on, not auto-included |

|---|---|

|

Lock Validity |

Up to 5 years from the purchase date |

|

Underwritten By |

Care Health Insurance |

|

Cost of the Add-On |

7% of the base plan premium annually |

|

Eligibility |

Available for DIC and Hayah policies across Dubai and Northern Emirates |

What are the Benefits of Premium Lock?

When you include the Premium Lock feature in your medical insurance policy, you can enjoy exclusive perks:

Protection Against Medical Inflation

Healthcare expenses are high in the UAE, and they even increase every year. Since insurers revise premiums based on rising healthcare costs, you may face higher renewal rates annually. Premium Lock saves you from these inflation-driven increases.

Avoid Age-Band Premium Hikes

Age plays a crucial role in deciding the premium. As you keep moving into higher age brackets, your premium tends to increase accordingly. Premium Lock freezes your premium at your entry age.

Long-Term Cost Savings

You save by avoiding yearly premium revisions. In fact, your cumulative savings can go beyond 40% over a 5-year period, depending on your age and premium structure.

Better Financial Planning

Since the premium remains fixed for a certain period, you can plan your finances more effectively without stressing out about insurance renewal increases.

Simple Add-On Structure

Premium Lock works as an add-on to your base health insurance policy. You simply pay:

- Base plan premium

- Premium Lock rider premium

Both remain fixed during the lock duration unless policy conditions are violated.

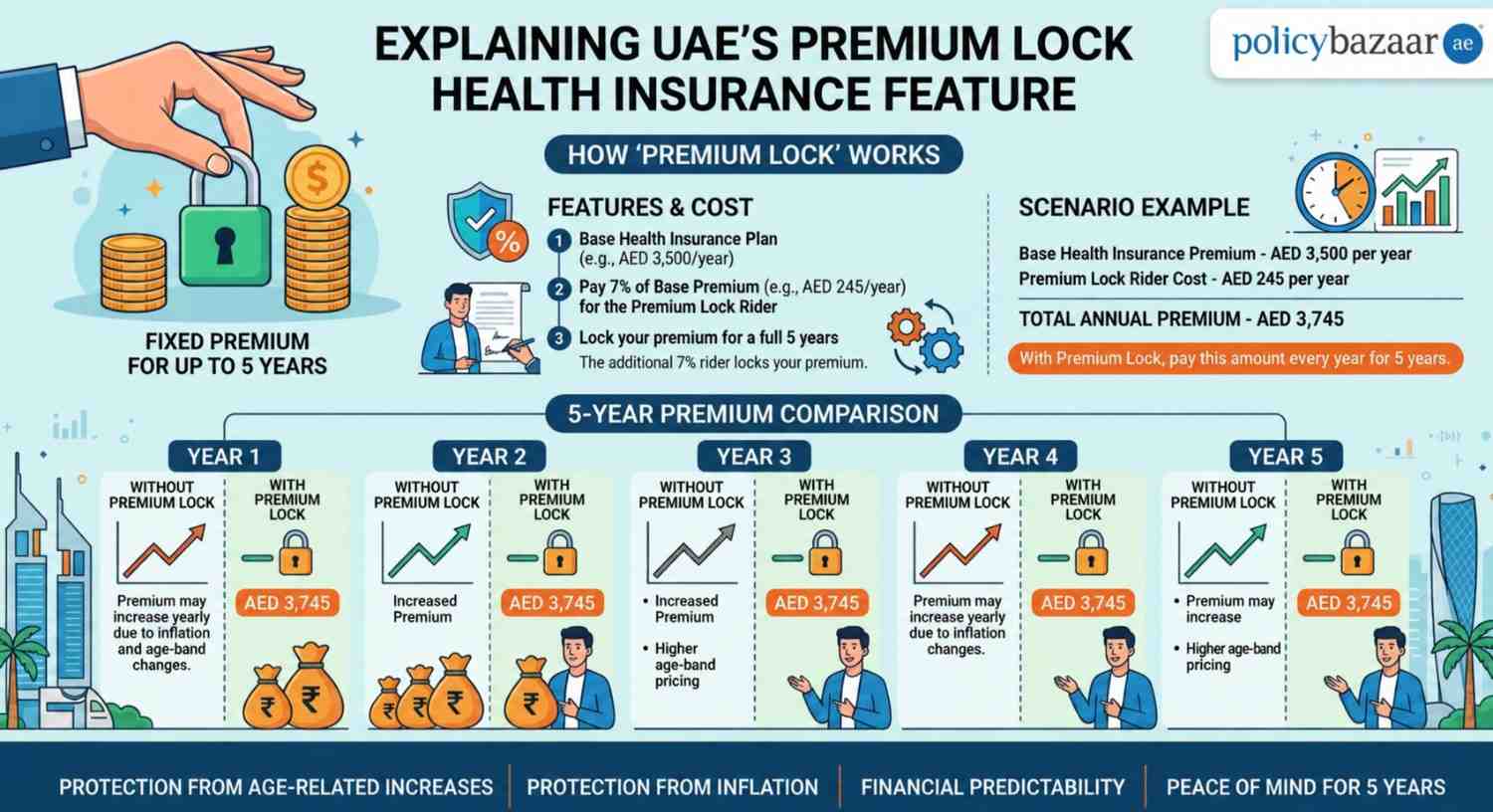

How Much Do I Need to Pay to Include the Rider in My Policy?

You can add Premium Lock to eligible health insurance plans on Policybazaar.ae at an additional cost of just 7% of the base plan premium per year. In return, your health insurance premium stays locked at the age you enrolled for up to five years. This protects you from annual medical inflation and age-band premium hikes that can increase renewal costs by 20–25%.

How Does the Premium Lock Work?

Premium Lock freezes your premium for up to 5 years from the date of purchase. However, the lock remains active only until the first inpatient hospitalisation claim is made or the 5-year period ends. Once the lock ends, normal renewal pricing applies again.

Example of How Premium Lock Works

Scenario

- Base Health Insurance Premium: AED 3,500 per year

- Premium Lock Rider Cost: AED 245 per year

- Total Annual Premium: AED 3,745

Without the add-on, the premium may increase yearly due to inflation and age-band changes. But with a premium lock, you continue paying AED 3,745 every year for 5 years.

Source- This image is AI-generated

Which Plans are Eligible for the Rider?

Premium Lock is applicable to Hayah and DIC health insurance plans (mentioned below) bought through Policybazaar.ae. However, regional eligibility applies. The add-on is currently available in Dubai and the Northern Emirates.

Eligible Plans

|

DIC Plans |

Hayah Plans |

|---|---|

|

✅ MedNet Standard ✅ MedNet NRI Care ✅ Dubai Care Standard ✅ Dubai Care NRI Care ✅ Care Next NRI Care ✅ Care Next Standard |

✅ Next Care Standard ✅ Next Care NRI Care ✅ MedNet Standard ✅ MedNet NRI Care |

Who Can’t Opt for Premium Lock?

The following category of individuals is not eligible for this add-on coverage:

Individuals Above 60 Years

Users aged above 60 years at the time of enrollment cannot purchase Premium Lock.

Policyholders with Pre-Existing Conditions Cover

If any insured member declares a pre-existing condition during policy purchase, the rider cannot be added.

Policies for Children

Standalone child policies do not qualify. The primary insured member must be an adult.

Customers Making Certain OPD Claims

The lock benefit may become void if:

- Maternity-related OPD claims are made

- Oncology or cancer-related OPD claims are made

Health Misdeclaration Cases

If an undeclared pre-existing condition is discovered later, the Premium Lock rider will be removed immediately, with no refund of the rider premium.

Is the Add-on Still Valid During Policy Renewal?

Yes, Premium Lock remains active during policy renewal for up to 5 years, provided all policy terms and conditions continue to be met. However, the lock may end if:

- An inpatient hospitalisation claim is filed

- The policyholder upgrades to a higher category plan

- The customer changes to another product line

- Regulatory changes introduce mandatory benefits with additional costs*

*In case of mandatory regulatory revisions, only the additional mandated cost may be added to the premium during the lock period.

Related Health Insurance

Is Premium Lock mandatory with health insurance plans?

No, Premium Lock is an optional add-on rider that you can choose while purchasing Hayah and DIC health insurance plans, exclusively on Policybazaar.ae.

How long does the Premium Lock benefit last?

The benefit remains active for up to 5 years or until the first inpatient hospitalisation claim is made, whichever happens earlier.

Does Premium Lock completely stop all premium increases?

No, premium lock does not completely stop all premium hikes. The rider protects against age-related premium increases and yearly inflation-based increases. However, note that premiums may still change if regulators include mandatory coverage in a base plan.

Can I use outpatient benefits while Premium Lock is active?

Yes, you can use the regular outpatient benefits. However, maternity-related OPD claims and oncology-related OPD claims discontinue the lock benefit.

Can customers with pre-existing diseases purchase Premium Lock?

No, customers declaring pre-existing conditions during policy purchase are not eligible for this add-on.

What happens after the 5-year lock period ends?

Once the lock duration ends, the policy moves back to standard renewal pricing based on age, insurer pricing, and medical inflation applicable at that time.

More From Health Insurance

- Recent Articles

- Popular Articles

Last Updated : 05 Aug 2026Buy Insurance in Installments UAE | 0% Interest via TabbySplit your health insurance premium into 4 monthly payments at 0% interest with Tabby. No minimum premium. Coverage starts day one. Available at Policybazaar.ae.

Last Updated : 05 Aug 2026Buy Insurance in Installments UAE | 0% Interest via TabbySplit your health insurance premium into 4 monthly payments at 0% interest with Tabby. No minimum premium. Coverage starts day one. Available at Policybazaar.ae. Last Updated : 09 Jun 2026How to Boost Immunity in Children Naturally | UAEBoost your child's immunity naturally with proper sleep, balanced diet, daily exercise, and timely vaccinations - no supplements needed in most cases.

Last Updated : 09 Jun 2026How to Boost Immunity in Children Naturally | UAEBoost your child's immunity naturally with proper sleep, balanced diet, daily exercise, and timely vaccinations - no supplements needed in most cases. Last Updated : 09 Jun 2026Digital Detox: Why Your Brain Needs a Break from ScreensDigital detox is a regular break from screens that reduces stress, improves sleep quality, and boosts productivity. Learn the signs you need one and how to start.

Last Updated : 09 Jun 2026Digital Detox: Why Your Brain Needs a Break from ScreensDigital detox is a regular break from screens that reduces stress, improves sleep quality, and boosts productivity. Learn the signs you need one and how to start. Last Updated : 08 Jun 2026PCOS Officially Renamed PMOS – What It Means for WomenPCOS is now officially PMOS – Polyendocrine Metabolic Ovarian Syndrome. Learn what this landmark 2026 name change means for 170 million women worldwide.

Last Updated : 08 Jun 2026PCOS Officially Renamed PMOS – What It Means for WomenPCOS is now officially PMOS – Polyendocrine Metabolic Ovarian Syndrome. Learn what this landmark 2026 name change means for 170 million women worldwide.-(2)-(2).webp) Last Updated : 03 Jun 202620-Minute Workouts for Busy Professionals | Stay Fit Fast4 proven 20-minute workout routines for busy professionals. HIIT, strength, office-friendly & fat-burning cardio — stay fit without long gym sessions.

Last Updated : 03 Jun 202620-Minute Workouts for Busy Professionals | Stay Fit Fast4 proven 20-minute workout routines for busy professionals. HIIT, strength, office-friendly & fat-burning cardio — stay fit without long gym sessions.-(2).webp) Last Updated : 03 Jun 2026Plant-Based Diet: Complete Guide to Benefits & FoodsA plant-based diet boosts heart health, weight loss, and immunity. Explore benefits, 5 food groups, and tips to get started in the UAE.

Last Updated : 03 Jun 2026Plant-Based Diet: Complete Guide to Benefits & FoodsA plant-based diet boosts heart health, weight loss, and immunity. Explore benefits, 5 food groups, and tips to get started in the UAE.

Last Updated : 10 Feb 2026How to Check Medical Insurance Status with Emirates ID?Emiratis will now be able to use their Emirates ID cards not only to go through immigration gates at the airport but to avail of medical services in the UAE.

Last Updated : 10 Feb 2026How to Check Medical Insurance Status with Emirates ID?Emiratis will now be able to use their Emirates ID cards not only to go through immigration gates at the airport but to avail of medical services in the UAE. Last Updated : 10 Jul 2026Best Health Insurance Companies in Dubai, UAE 2026Find the Top 10+ Health Insurance Companies in Dubai, UAE Offering Comprehensive Health Insurance Coverage and Exceptional Services at Affordable Prices.

Last Updated : 10 Jul 2026Best Health Insurance Companies in Dubai, UAE 2026Find the Top 10+ Health Insurance Companies in Dubai, UAE Offering Comprehensive Health Insurance Coverage and Exceptional Services at Affordable Prices. Last Updated : 26 May 2026How to Check the Status of Your Health Insurance Online?The easiest way to get familiar with your plan details or check the active status is to do it online. Let’s figure out how to check if your health insurance plan is active online.

Last Updated : 26 May 2026How to Check the Status of Your Health Insurance Online?The easiest way to get familiar with your plan details or check the active status is to do it online. Let’s figure out how to check if your health insurance plan is active online. Last Updated : 08 Jan 2026Dental Insurance UAE: Dental Insurance Types, Coverage & BenefitsDental Insurance UAE: Know All about Dental Insurance, Types, Coverage & Benefits. Dental Insurance Covering Most of the Dental Treatments, You can Drop off Your Worries About Costly Therapies.

Last Updated : 08 Jan 2026Dental Insurance UAE: Dental Insurance Types, Coverage & BenefitsDental Insurance UAE: Know All about Dental Insurance, Types, Coverage & Benefits. Dental Insurance Covering Most of the Dental Treatments, You can Drop off Your Worries About Costly Therapies. Last Updated : 11 Feb 2026Can You Buy Health Insurance for New Born Baby in UAE?Don't know whether you can buy medical insurance for new born baby in UAE? In this article we’ll share everything you need to know about health insurance for newborn baby.

Last Updated : 11 Feb 2026Can You Buy Health Insurance for New Born Baby in UAE?Don't know whether you can buy medical insurance for new born baby in UAE? In this article we’ll share everything you need to know about health insurance for newborn baby. Last Updated : 27 Nov 2025Where Can I Get Medical Help Without Having Health Insurance in UAE?Not everyone in the UAE can afford to buy a health insurance policy to avail of quality medical care benefits. To help out such people, we have listed here a few places and ways of getting medical help.

Last Updated : 27 Nov 2025Where Can I Get Medical Help Without Having Health Insurance in UAE?Not everyone in the UAE can afford to buy a health insurance policy to avail of quality medical care benefits. To help out such people, we have listed here a few places and ways of getting medical help.